Parking Lot Resurfacing Depreciation

Solved Kim S Asphalt Does Driveway And Parking Lot Resurf Chegg Com

Solved Kim S Asphalt Does Driveway And Parking Lot Resurf Chegg Com

Solved Kim S Asphalt Does Driveway And Parking Lot Resurf Chegg Com

What Every Property Owner Should Know About Parking Lot Resurfacing

Solved Rin S Asphalt Does Driveway And Parking Lot Resurf Chegg Com

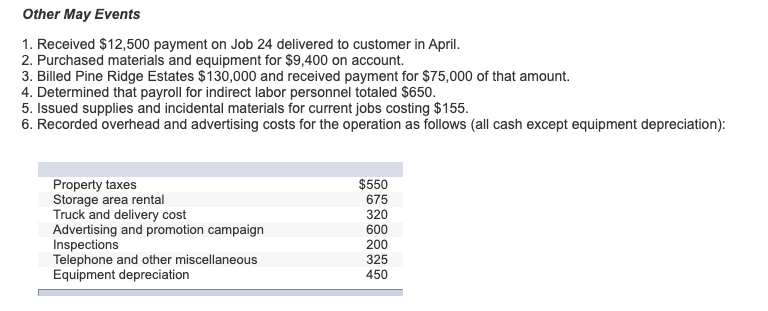

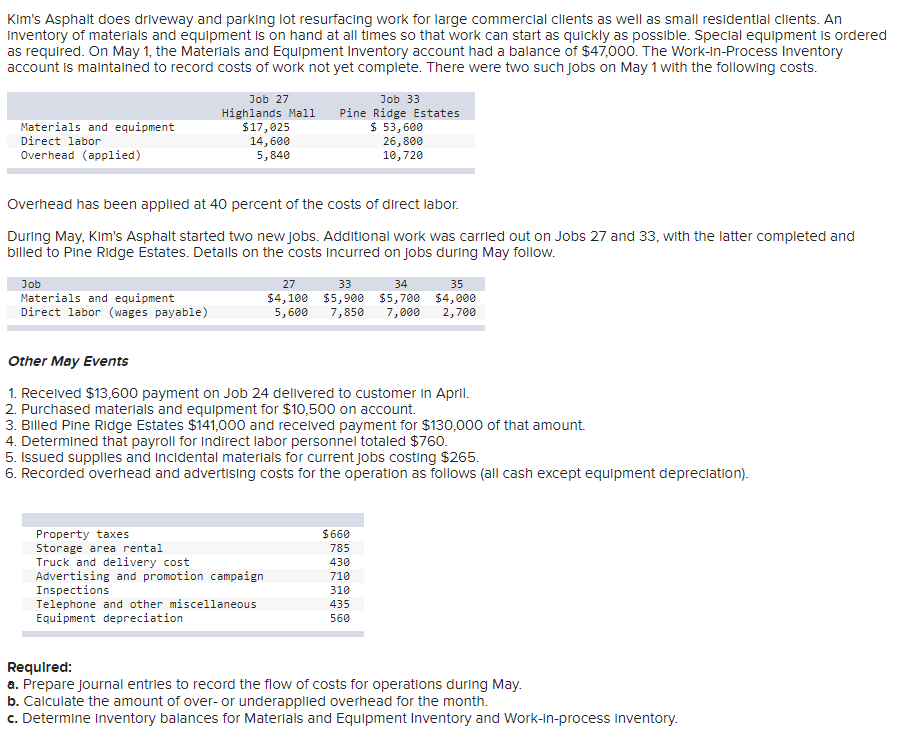

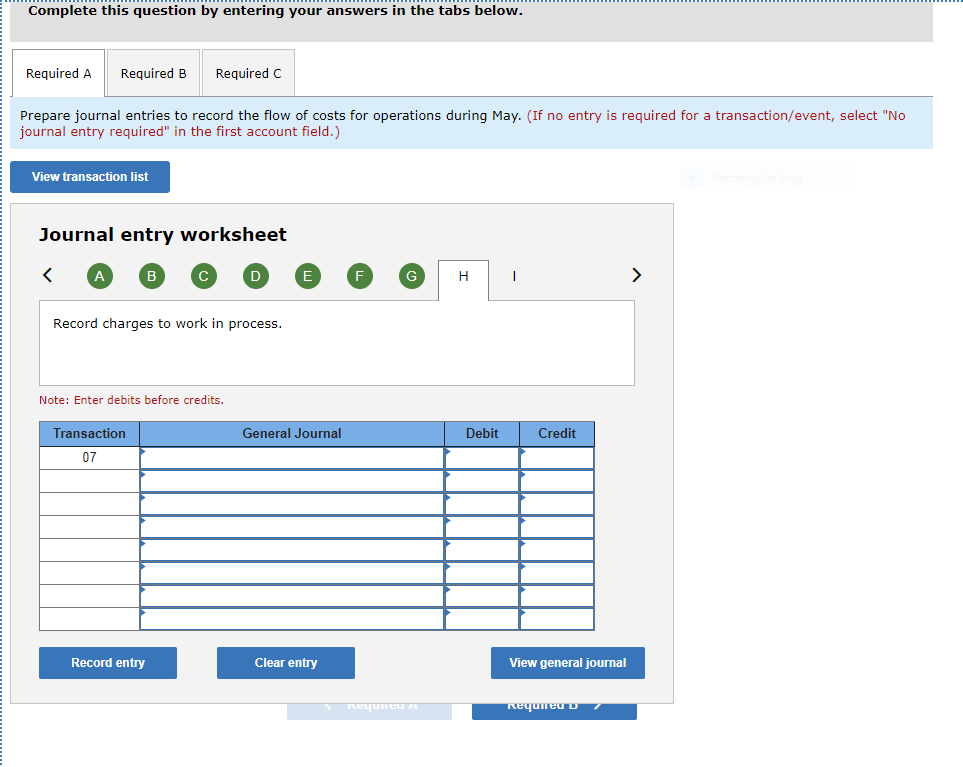

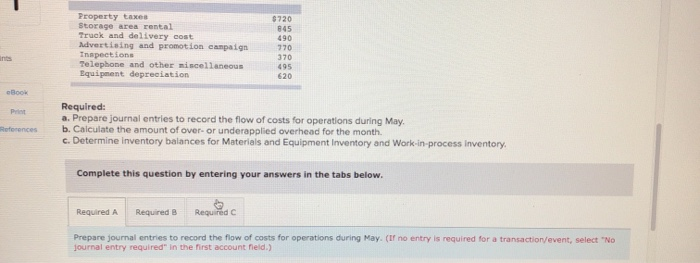

Solved Problem 7 53 Show Flow Of Costs To Jobs Lo 7 2 3 Chegg Com

A business owner can take a depreciation off his taxes for a paved driveway he put in to improve his facilities.

Parking lot resurfacing depreciation.

When Should You Repave A Parking Lot Wolf Commercial Real Estate South Jersey Philadelphia Pa

Kim S Asphalt Does Driveway And Parking Lot Resurf Chegg Com

Tyumpk39dffbm

Actual Overhead Amounted To 520000 With Actual Machine Hours Totaling 45500 Course Hero

40 Points Kim S Asphalt Does Driveway And Parking Chegg Com

Rytnebgc1f Pdm

Unlocking Hidden Tax Benefits In Your Apartment Investments By Jeff Glass Aoa Magazine

Solved Oriole Machining Purchased The Assets Of An Existi Chegg Com

Tax Reform Nondeductible Parking Expenses And Their Impact On Your Business Ksm Blog Katz Sapper Miller Cpa

Tangible Property Treatment Analysis Engineered Tax Services Inc

Parking Lot Maintenance Tips Sable Asphalt Akron Oh

Curb Painting For Parking Lots In Knoxville Tn 865 680 9225 Parking Lot Striping Sealcoating Parking Lot Striping Urban Landscape Design Parking Lot Painting

Pavement Repair 865 680 9225 Parking Lot Striping Handicap Stencil Painting Asphalt Paving C Parking Lot Striping Asphalt Paving Contractors Paving Contractors

Https Clearlawinstitute Com Webinars The Complete Guide To Depreciation And Amortization 2 Cli The Complete Guide To Depreciation Amortization

Pavement Repair 865 680 9225 Parking Lot Striping Handicap Stencil Painting Asphalt Paving Contractor Pavement Sealing Sealcoating Resurfacing

Https Www Newingtonct Gov Documentcenter View 8215 2020 2021 Proposed Cip Pdf

Https Www Lexingtonky Gov Sites Default Files 2018 04 Cao 20policy 2047 Pdf

Implementing The New Tangible Property Regulations

Https Www Findlayohio Com Home Showdocument Id 7373

Cost Segregation And Tangible Property Repair Regulations

Parking Lot Freshly Paved Asphalt Repair Paving Contractors Asphalt Pavement

Https Www Vtpi Org Park Man Comp Pdf

Parking Area Painting 865 680 9225 Sealcoating Resurfacing Loy Striping Lenoir City Knoxville Tn Parking Lot Striping Lenoir City Driveway Paving

Paved Parking Lot Bloomington Indiana Paving Bloomington

Source : pinterest.com