Parking Lot Resurfacing Capitalize Or Expense

Budgeting Maintenance Costs In Parking Structures

How To Start A Parking Lot Business

Restaurant Parking Lots Does Yours Contribute To The Business Plan Kansas Asphalt Inc

How To Care For Parking Lots In Freeze Thaw Conditions Bluefin Roof Walls Pavement And Energy Consultant

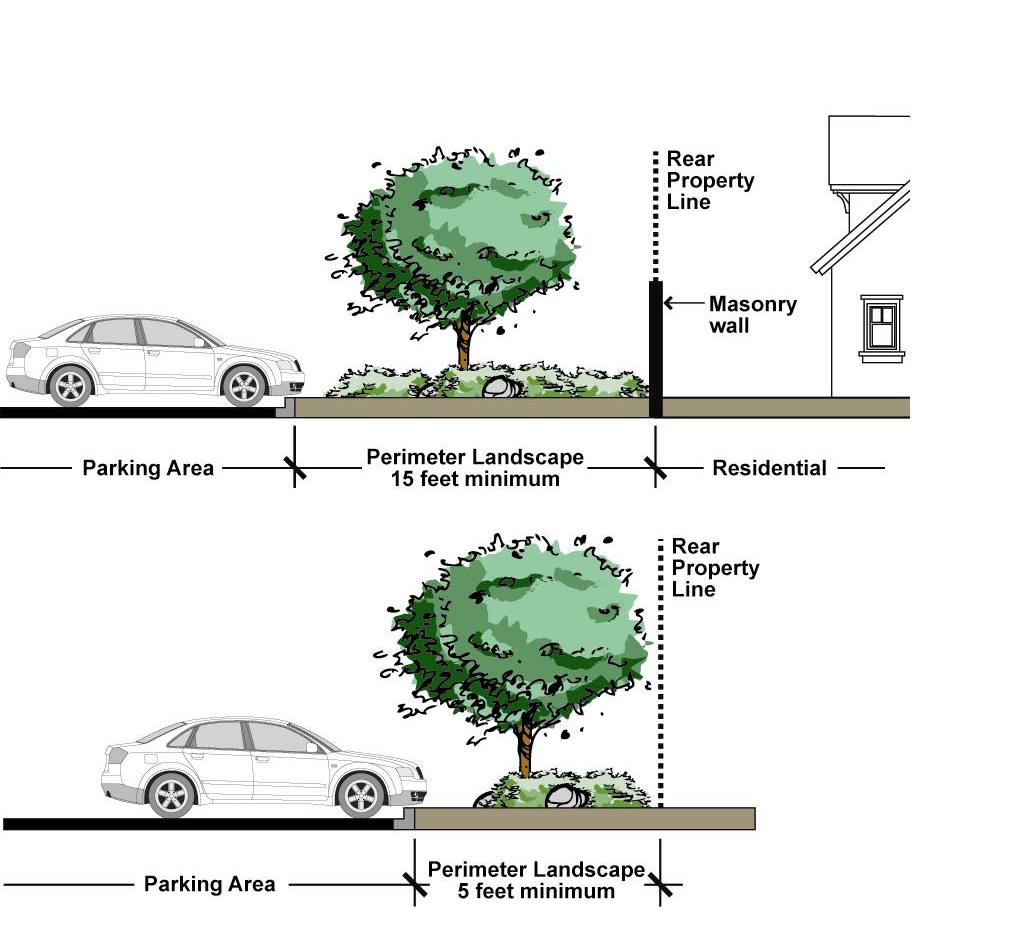

Chapter 19 38 Off Street Parking Regulations And Design Development Code Duarte Ca Municode Library

Quick Easy And Permanent Asphalt Repair And Parking Lot Repair Is Possible Asphalt Repair Repair Parking Lot

For more details on current vs.

Parking lot resurfacing capitalize or expense.

Parking Fees Explained Livegreen

Glen Ellyn Park District Established In 1919 Glen Ellyn Illinois

Drivers At Thomas Jefferson Houses In East Harlem Hit By 353 Parking Rate Hike Thomas Jefferson Emergency Vehicles Jefferson

Https Www Co Walton Fl Us Documentcenter View 3235 Ldc Chapter 5 Design And Development Standards Bidid

High School Parking Lot Pothole Parking Lot Repair Asphalt Repair

Http Zoningpgc Pgplanning Com Wp Content Uploads 2016 05 Final Prd Pgc Mod 2 Div 27 5 05 09 16 Pdf

Securing Church Loans For Your Church Building Loan Church Church Building

How To Start A Parking Lot Business Small Business Chron Com

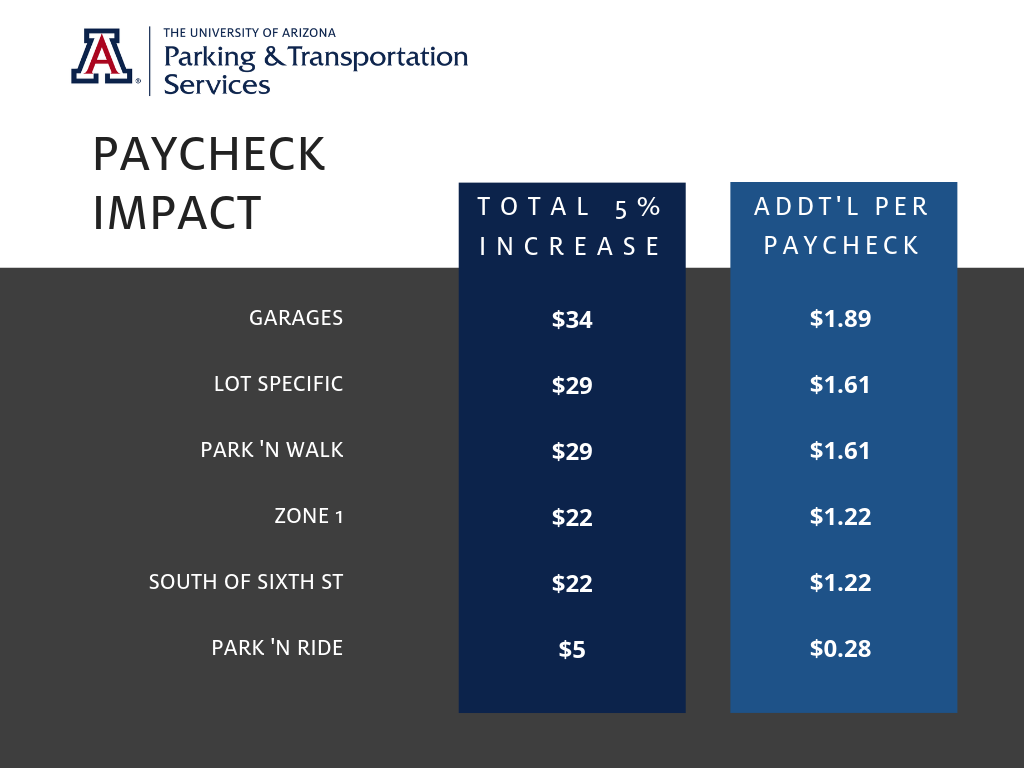

Ua Pts Program Update Parking Permit Rates 2019 2020

Palo Alto Looks To Launch Safe Parking Program For People Living In Cars News Palo Alto Online

Download A Free Home Inspection Checklist Template For Excel Or A Printable Home Inspection Form In Pdf Form In 2020 Inspection Checklist Home Inspection Selling House

Full Depth Reclamation For Parking Lot Paving For Construction Pros

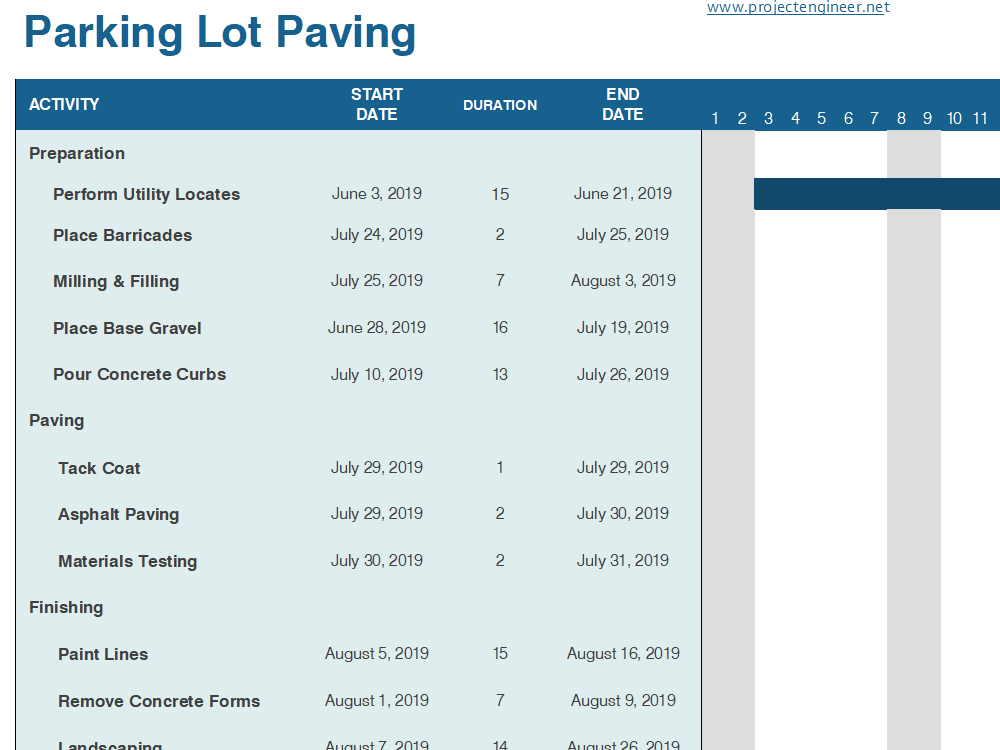

10 Gantt Chart Templates Beautiful Professional And Free

Pin On Budget Template

What Are The Options For Parking Lot Sealcoating Aexcel

The Detailed Cost Breakdown To Building A New Parking Garage

Schedule C Excel Template Awesome Schedule C Expenses Template Along With Elegant Business In 2020 Small Business Expenses Business Expense Tracker Business Expense

Budget Status Budget Report Template Budget Report Template Should Be Chosen Well And Should Be Conducted For Get Budgeting Budget Template Report Template

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcruudquawzq E8mbyb4ke2znmciekdhtocmlfmspcbkckelszxd Usqp Cau

The Magical World Where Mcdonald S Pays 15 An Hour It S Australia Food Cost Mcdonalds Franchise Restaurants

Eat Live Make Living Well With Less 5 Ways To Make Every Dollar Count Ways To Save Money Living Well Ways To Save

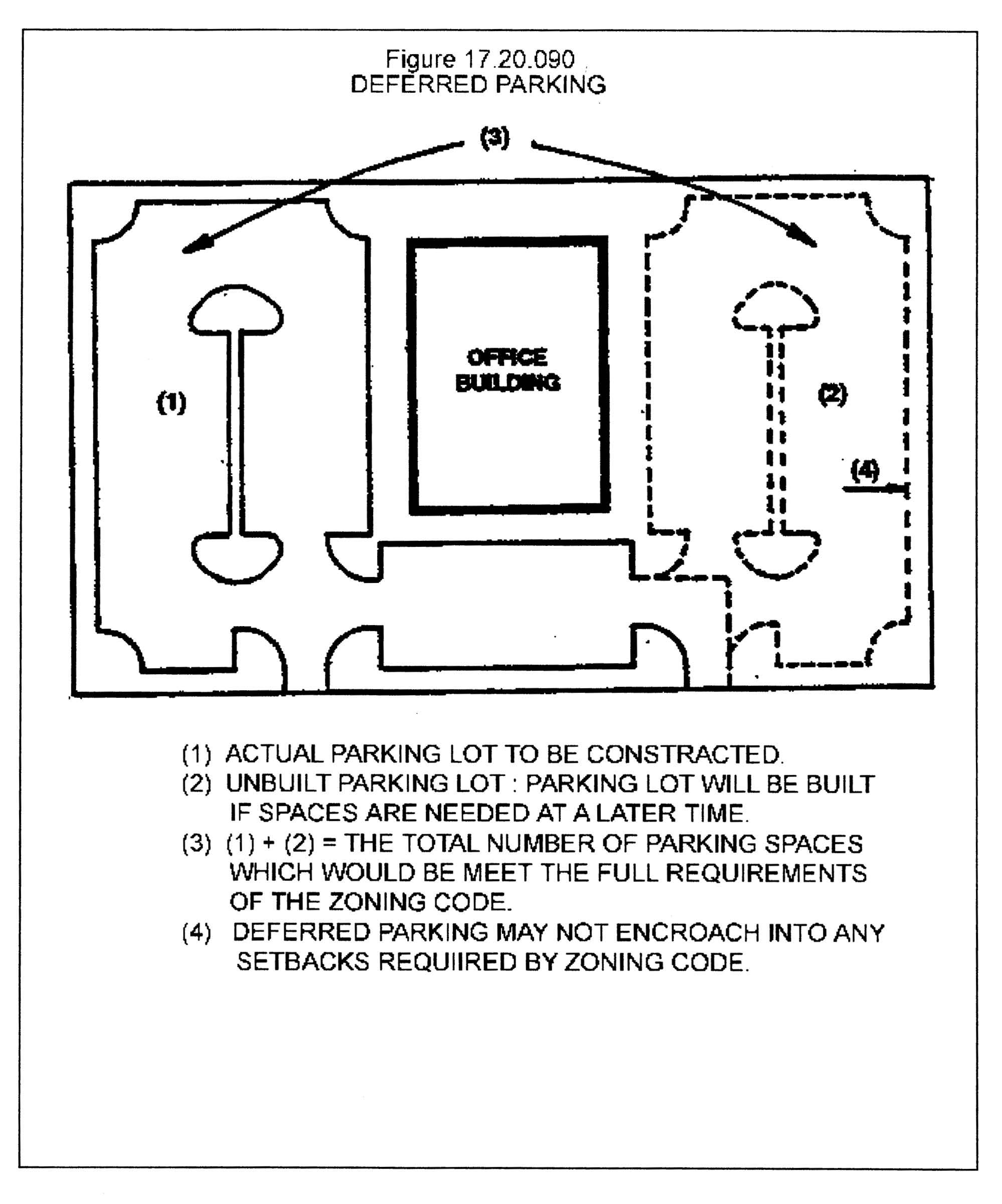

Chapter 17 20 Parking Loading And Access Code Of Ordinances Metro Government Of Nashville And Davidson County Tn Municode Library

Three Examples Of Sole Proprietorships Ehow Search Results In 2020 Balance Sheet Balance Sheet Template Sole Proprietorship

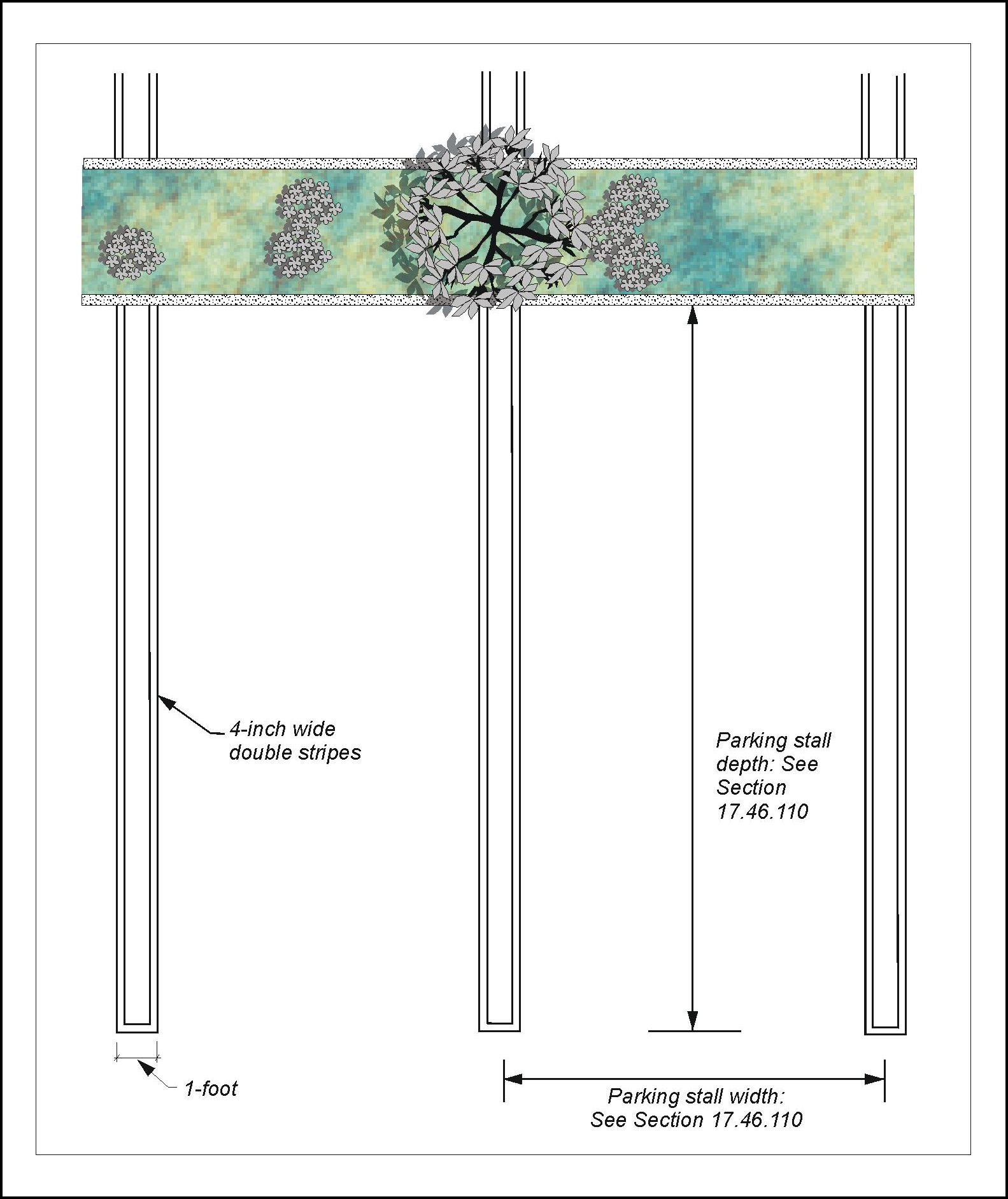

Chapter 17 46 Parking And Loading Code Of Ordinances Pasadena Ca Municode Library

Source : pinterest.com